FICO scores, credit reports, and mortgages

When it comes to securing a mortgage it’s important to understand your FICO score, where it comes from and most importantly, what score you need to qualify for a home loan. Here’s a complete breakdown of FICO scores, how they affect your credit report and an exact breakdown of what credit score you need to qualify for a mortgage. To learn more about the application, about the 4 easy steps to getting a mortgage loan.

WHAT IS A FICO SCORE?

Your FICO score is a number that represents your reliability and creditworthiness – how likely you are to pay back your debts if you borrow from a lender. The FICO score is a credit score, the most widely used in fact in the U.S.

FICO = Credit Score

HOW IS A FICO SCORE GENERATED?

Loan officers and real estate financial advisors have access to mortgage underwriting systems. First you will run your credit through 3 credit repositories: Experian, Equifax and Tansunion (you can run these credit reports for free online). If you need to improve your credit score try these 9 simple tips.

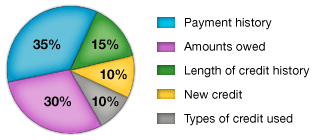

Here’s how these respositories come up with your FICO score:

35% – Payment History

The largest portion of your FICO score is determined from whether or not you have “derogatory information” in your credit history. Bankruptcy, late payments, foreclosures, etc. will lower your FICO score.

30% – Debt Burden

This is most commonly known as your debt-to-income ratio. The lender is looking at how much income you bring in and the amount of money you owe on credit accounts currently. There are a lot of other little pieces that play into this part of determine your FICO score however.

Underwritings systems also look at:

Amount owed on your credit cards (current balance).

The type of accounts you have i.e. credit cards and long term loans.

How many accounts have balances. The more you have, the higher the risk for lenders.

How you use your credit accounts – Using a lower ratio of your credit limit is better and showing consistently well-managed payments is a plus.

How much you’ve paid on standing installment loans – Paying down installment loans (like a car payment) is a good sign that you’re financially responsible and able to pay future debts.

15% – Time

The longer your credit history, the better. The underwriting systems look at the average age all accounts as well as the age of the oldest account.

10% – Types of Credit

Diversity is good! Managing several different types of credit like installment, revolving and consumer finance credit can be beneficial to your score.

10% – Recent Searches

Too many recent searches can hurt your credit score, most importantly hard searches done by lenders when you apply for a new credit card or loan. Keep in mind that the FICO score does take into consideration rate shopping so if you check your score several times over a short period of time (14-45 days to be exact),it will only appear on your report as one inquiry.

WHAT CREDIT SCORE DO YOU NEED TO QUALIFY FOR A MORTGAGE?

Once you have your FICO score it’s time to consult with a real estate financial advisor or loan officer. They will run your credit score and full information into underwriting systems to see who will accept you loan and what type of loan and rates you’re eligible for. Only accredited financial professionals have access to these underwriting systems. What credit score you need to qualify for a mortgage depends on whether you choose a Conventional or FHA loan. Haven’t decided yet? Check out our complete price breakdown of FHA vs. Conventional financing.

CONVENTIONAL LOANS:

780 and above– Qualify for the best rate available

700-779 – Qualify for a relatively good rate. It will not be as low as someone with the highest score possible but it will be good.

660-700 – Qualify for an average rate. It won’t be the best rate on the market but you will be able to qualify.

650 and below – May qualify for a higher rate depending on the size of your down payment. Those with a higher down payment are more likely to qualify.

FHA LOANS:

620 and above – Qualify for a mortgage loan with 3.5% down. FHA lending standards not as strict as Conventional loans however lenders are tightening their restrictions.

580-620 – May qualify with a 10% down payment.

Nontraditional Credit – May qualify with 3 valid credit references. If you have limited credit or none at all, FHA will accept 3 positive credit references i.e. consistent utility payments, cell phone bill, gym membership, etc.

Still have questions about your credit score and how to secure a mortgage? Team up with an agent to help you. You can search for a First Team agent on our site or let us connect you with one. Call 888-870-1142 or email us at clientservices@firstteam.com and we’ll set you on the road to a mortgage loan and homeownership today.

Originally posted at: ow.ly/zID82